At its core, a cross-border payment solution is simply the technology that lets people and businesses send money from one country to another. These systems are the backbone of the global economy, making everything possible from a freelancer in Argentina getting paid by a client in Spain to a global platform like Klink distributing rewards to users worldwide.

Sending Money in a Borderless World

In today's world, where you live no longer dictates where you can earn. A designer in the Philippines can create a logo for a startup in Germany, or a gamer in Brazil can cash out earnings from a US-based app. In every case, money needs to move across borders.

This is where cross-border payment solutions come in. Think of them as the engine that powers this global flow of money. They’re the infrastructure that ensures funds sent from one country arrive safely in another, navigating different currencies, banking rules, and regulations along the way.

The Old Way vs. The New Way

Not long ago, sending money internationally was a painful process. It was slow, expensive, and anything but transparent. Traditional bank wires would bounce between several intermediary banks, with each one taking a slice of the pie and adding days to the transfer time.

This old model was a massive headache for everyone. Businesses struggled to pay their global teams on time, and individuals were left waiting for money they’d already earned.

Thankfully, modern financial technology has completely changed the game. Today’s solutions are built for speed, clarity, and flexibility, knocking down the old barriers that made global payments so difficult. This shift is especially crucial for platforms that need to send lots of small payments to a huge number of users scattered across the globe.

The total value of cross-border payments hit an incredible US$190 trillion in 2023. That number shows just how massive the global economy is—and why efficient payment systems are no longer a nice-to-have, but a must-have.

Empowering Global Earners

This evolution is exactly what makes a platform like Klink Finance possible. Klink is a global rewards platform where users earn real money for doing things like completing simple online tasks, playing games, or trying out new services. The entire system relies on one critical function: the ability to pay out those earnings instantly and reliably, no matter where a user lives.

By using modern cross-border payment solutions, Klink turns online activities into real, spendable cash without the usual headaches. This means users can:

Earn Globally: Access offers from brands and partners all over the world.

Withdraw Flexibly: Cash out their earnings into different currencies, like USD or EUR.

Get Paid Fast: Skip the long delays that come with old-school banking.

This guide is your roadmap to understanding how it all works. We’ll break down the different payment systems, look at the options available, and show you how to navigate the world of borderless payments—whether you’re a platform paying users or an earner getting paid.

How Cross-Border Payments Actually Work

To understand cross-border payment solutions, think of them as international shipping services for your money. Some are like express air freight—incredibly fast but more expensive. Others are like slow sea cargo—cheaper, but the journey takes much longer. These solutions are the complete system of technology, networks, and rules that get money from a bank or wallet in one country to another.

At first glance, sending money looks like a simple click. Behind that click, however, is a complex chain of events involving multiple players, each with a specific job. This system is what ensures every single transaction is secure, accurate, and compliant with a web of international laws.

For a global rewards platform like Klink Finance, this system’s reliability is non-negotiable. Klink enables a global community of users to earn by completing online tasks, and those users expect to get paid instantly. The platform's entire success hinges on a payment infrastructure that works flawlessly, every single time, delivering funds quickly and accurately across dozens of countries.

The Key Players in a Global Transaction

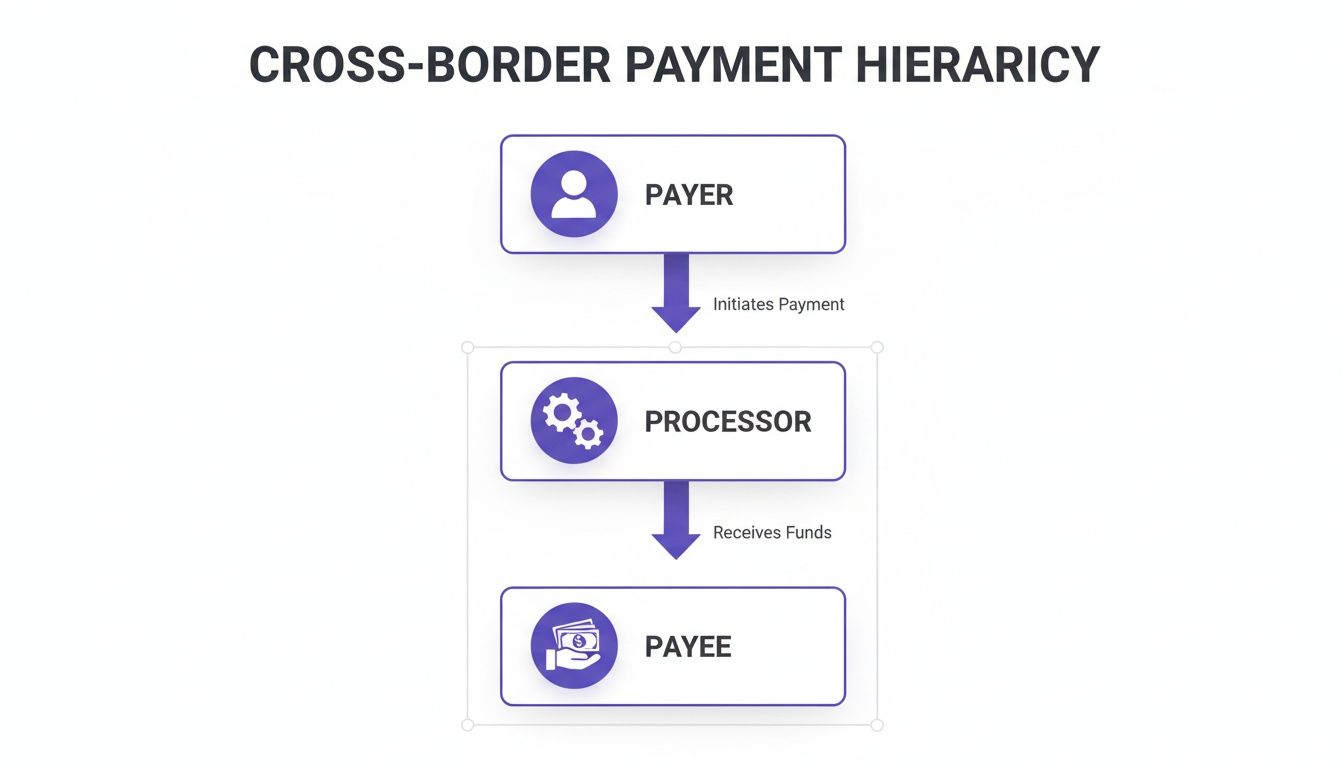

Every time money crosses a border, a team of financial institutions works behind the scenes. While the specific players can change, most international transactions involve a similar cast of characters.

The Sender (Payer): This is the person or business kicking off the payment. It could be a company paying an international freelancer or a platform like Klink paying out user earnings.

The Sending Institution: This is the payer's bank or payment service provider (PSP). They are responsible for starting the transfer and debiting the funds from the sender's account.

Payment Processors & Networks: These are the intermediaries—the highways for the money. They process transaction details, handle currency conversions, and route funds between different banks and countries.

Receiving Institution: This is the bank or PSP on the other end. Their job is to accept the incoming funds and credit them to the recipient's account.

The Recipient (Payee): This is the final destination—the person or business receiving the money.

This chain of communication and fund movement is what makes sending money around the world possible.

A Simple Analogy: The International Relay Race

Imagine sending money as a relay race. The sender hands the baton (the money and transaction data) to their bank. That bank then passes it to an international payment network, which runs it across the border to the recipient's bank. Finally, the recipient's bank hands the baton to the end user.

In this race, every handoff must be perfect. Any mistake, delay, or miscommunication can cause the entire transfer to fail or get stuck. This is why robust cross-border payment solutions are so critical—they act as the coaches and rule-keepers, making sure the race runs smoothly from start to finish.

This process highlights just how important every link in the chain is. From verifying the sender's identity to clearing the funds through multiple banking systems, each step is designed to protect against fraud and ensure the money arrives securely.

Why This Matters for Platforms and Earners

If you run a platform that pays a global user base, understanding this process is crucial for choosing the right payment partner. A solution that is slow, unreliable, or has high fees creates a terrible user experience. It leads to frustrated users who abandon your platform because they can't get their earnings easily.

For the earners themselves, this system directly impacts how quickly they get paid. That's why platforms like Klink Finance prioritize modern, efficient payment solutions that cut down on the number of handoffs and speed up the whole process. By doing so, they turn a potentially week-long wait into an instant payout, making the experience of earning online seamless and rewarding.

Understanding the Different Payment Rails

Think of cross-border payment solutions as different highways for your money. Each highway, or "payment rail," has its own speed limits, toll costs, and destinations it can reach. When you need to send money from one country to another, it has to travel on one of these rails to get from point A to point B.

Picking the right one is a big deal. The rail you choose directly impacts how fast the money arrives, how much gets skimmed off in fees, and how easy it is for the person on the other end to actually get their cash. Some of these rails are built on ancient infrastructure, while others were designed for the speed of today's internet.

This diagram shows the typical journey. Money rarely goes straight from sender to receiver. It hops between a few intermediaries first.

Those hops are often where the delays and surprise fees pop up. Let's break down the most common payment rails you'll encounter.

The Main Payment Rails

There are three primary ways money moves across borders. Each comes with a different set of trade-offs in speed, cost, and global reach.

1. Traditional Bank Wires: The Reliable Workhorse

The oldest and most established route is the traditional bank wire system, powered mostly by the SWIFT network. Think of SWIFT as the global postal service for banks. It doesn't actually move the money itself, but it sends secure payment messages between its 11,000 member institutions around the world.

This system is incredibly reliable and can handle huge sums, which is why it’s the go-to for big corporations and banks. But for everyone else, it has some serious drawbacks.

Speed: Wires are slow. A payment can take 3 to 5 business days to clear because the message often has to hop between several "correspondent" banks before it gets to the final destination.

Cost: Each of those bank-to-bank hops can come with a fee. This leads to high, and often unpredictable, costs that get deducted from the amount your user receives.

For a platform paying out small, frequent rewards to a global user base, relying only on bank wires would be a nightmare of high fees and long waits. It’s just not built for that.

2. Card Networks: The Consumer Favorite

Everyone knows Visa and Mastercard. We use them every day online and in stores. For paying a business, they’re fast, convenient, and incredibly familiar. They’re a massive, powerful payment rail.

But things get a little trickier when a business needs to pay a person. Sending money directly to a user's debit or credit card—a process called an "original credit transaction" (OCT)—isn't available everywhere and often comes with its own set of rules and fees.

While fantastic for collecting payments, card networks weren’t originally built for mass global payouts. They're a useful piece of the puzzle, but not a complete cross-border payment solution for most modern platforms.

3. E-Wallets and Fintechs: The Modern Alternative

This is where things have gotten really interesting. Fintech companies have built entirely new payment rails designed to fix the problems with the old systems. Think of them as digital shortcuts that offer faster speeds at a fraction of the cost.

So, how do they do it? Many of these providers maintain a network of local bank accounts in dozens of countries. This clever setup allows them to treat an international payment like a simple local transfer, dodging the slow and expensive correspondent banking system entirely.

For a global platform like Klink Finance, this kind of flexibility is everything. As a global rewards platform where users earn real money by completing online tasks or playing games, we’re obsessed with giving our users instant, no-hassle access to their earnings. We make that happen by strategically blending different payment rails to offer a menu of payout options.

By giving users a choice, Klink ensures they can pick the cheapest and most convenient way to withdraw their money, no matter where they are. Someone in Europe might want a direct SEPA transfer in EUR, while a user in Asia might prefer something else entirely. Our system is built to handle both. It puts the user back in control.

Modern payment tech is also where AI is making a huge difference in optimizing which rails to use for any given transaction. You can learn more about this in our guide on how AI and new financial systems work together.

Comparing Cross-Border Payment Rails

To make it easier to see the differences, here’s a quick comparison of the main rails.

Payment Rail | Average Speed | Typical Cost | Best For |

|---|---|---|---|

Bank Wires (SWIFT) | 3-5 business days | High ($25 - $50+) | Large, infrequent corporate transactions; high-security payments. |

Card Networks | Near-instant to 3 days | Moderate (1-3% + fixed fees) | Consumer purchases; limited B2C payouts in supported regions. |

E-Wallets/Fintech | Minutes to 24 hours | Low (often a small percentage or flat fee) | Mass payouts, freelancer payments, small-to-medium transfers. |

As you can see, there’s no single "best" option. The right choice depends entirely on what you're trying to do—whether you're sending a million-dollar corporate transfer or a $10 gaming reward. The smartest platforms don't just pick one; they use a mix to get the best results.

Navigating the Hidden Costs and Complexities

Even with modern cross-border payment solutions, the path money takes from one country to another is rarely a straight line. It’s a journey filled with potential traps—from sneaky fees that chip away at the total to baffling delays and rigid legal hurdles.

Understanding these challenges is the first step to appreciating why a clean, transparent payment experience is so critical.

The sheer scale of these transactions is staggering. In 2023, the total value of cross-border payments hit US$190 trillion, a figure projected to climb to US$290 trillion by 2030. Yet, businesses are stuck paying over US$120 billion in fees every year just to move that money. That's a massive amount of friction in the system.

For the people actually earning on global platforms, these costs turn a good payday into a frustrating mystery. It’s exactly this problem that a platform like Klink Finance is built to solve. As a global rewards platform, Klink enables users to earn real money by completing tasks and playing games. We handle the messy backend of payments so our users don't have to.

Unpacking the Real Cost of Sending Money

The most common complaint about international payments? The amount that arrives is less than the amount that was sent. This isn't just about the advertised transfer fee; a series of "hidden" charges often takes a bite out of the money along the way.

Currency Conversion Markups: When you convert USD to EUR, for instance, you rarely get the mid-market rate you see on Google. Instead, banks and providers use their own inflated rate, adding a small percentage on top as their profit.

Intermediary Bank Fees: As we covered, traditional wire transfers often hop between several "correspondent" banks before reaching their destination. Each one of those banks can skim a handling fee right off the top.

Receiving Fees: Believe it or not, some banks will even charge the recipient a fee just for the privilege of accepting an international payment.

Each cut might be small, but they add up fast, creating a real gap between what you expect and what you actually get.

Why Do Some Payments Take So Long?

The other major headache is the unpredictable timing. While some fintech solutions are nearly instant, many payments still crawl through ancient infrastructure, leading to delays for a few common reasons. To really get it, it helps to understand what a SWIFT payment is—it’s one of the oldest and most widely used rails, and it’s not known for its speed.

The journey of a cross-border payment is often interrupted by different time zones, banking holidays, and manual processing checks. A transfer initiated on a Friday in New York might not even begin its journey until Monday morning in London.

A bank holiday in either the sending or receiving country can freeze a payment for an entire day. On top of that, most banks have "cut-off times," meaning if you send a payment after 2 PM, it won’t even start moving until the next business day. It's a logistical puzzle that almost guarantees delays.

The Non-Negotiable World of Compliance

The biggest and most complex hurdle, however, is regulatory compliance. To fight financial crime, governments impose strict rules on anyone moving money. These aren't just suggestions; they are serious legal requirements designed to keep the financial system safe.

Two of the most important concepts here are:

Anti-Money Laundering (AML): These are the procedures that stop criminals from washing illegally obtained funds through legitimate channels. Payment providers have to monitor every transaction for red flags.

Know Your Customer (KYC): This is just what it sounds like—verifying a user's identity. Platforms must collect and confirm details like a person's name, address, and government ID before they're allowed to send or receive money.

These checks are absolutely essential for security, but they add a ton of friction. They take time, technology, and specialized expertise to get right, creating a huge operational lift for any platform paying users around the world. We dive deeper into how this is managed in our post on how Klink Finance prioritizes security.

Platforms like Klink Finance are designed to absorb all of this complexity—the hidden fees, the processing delays, and the compliance burden. By handling it all behind the scenes, we can give earners a simple, transparent experience focused on one thing: getting their money, fast and in full.

Choosing the Right Solution for Your Platform

Picking a partner for global payouts isn’t just a tech decision—it’s a strategic one. Get it right, and it feels like a seamless extension of your platform. Get it wrong, and you're stuck with user complaints, operational headaches, and stunted growth.

The goal is to find a solution that quietly handles the messy parts of international finance so you can stay focused on your actual product. But here’s the thing: there is no "best" solution. There's only the best solution for you.

Key Factors to Consider

Before you even start looking at providers, you need to understand your own payment DNA. Answering a few straightforward questions will give you a blueprint for what you actually need.

Who are you paying? Seriously, who are they? Are your users clustered in a few key countries, or are they spread all over the globe? Do they live and die by bank transfers, or are they expecting local e-wallets? You have to meet them where they are.

What are you paying? Think about the flow. Are you sending a few large, infrequent transfers? Or are you processing thousands of tiny micropayments every single day? A platform built for high-volume, low-value payouts needs a completely different cost structure.

How will it integrate? Your developers will thank you for this one. The solution must plug into your existing systems without a six-month engineering nightmare. A clean, well-documented API isn't a "nice-to-have"—it's a deal-breaker.

Can it scale with you? You’re building a business to grow. Your payment infrastructure has to be ready for that. Will it buckle when you 10x your user base, or will it handle the surge without breaking a sweat?

A critical part of this infrastructure is the payment gateway. Understanding the technical side is important, and a helpful guide to payment gateway software development can provide valuable context on how these systems are built to handle secure transactions.

Aligning Solutions with Your Business Model

The global payments market is exploding. Right now, it's a USD 371.59 billion market, and the Asia-Pacific region is leading the way with a whopping 46.30% market share. Analysts expect it to more than double by 2034, which is a massive opportunity for platforms that can master global payouts.

Klink Finance is a great real-world example. As a global rewards app, we let users earn real money by doing things like playing games or completing online tasks. This means we send a huge volume of small, instant payments to users all over the world.

For a model like ours, the payment infrastructure absolutely must be:

Fast: People complete a task, they want their money. Now. Any delay kills trust and makes the app feel clunky.

Low-Cost: If transaction fees eat up a significant chunk of a small reward, the entire value proposition falls apart.

Automated: You can't manually process thousands of payments a day. It’s just not possible. The system has to run itself.

By building our payout system around these three pillars, we make sure the user experience is smooth and rewarding. That’s what keeps our community of online earners coming back.

In the end, this is about finding a partner who gets your specific challenges and has the tech to solve them. It's less about buying a product and more about finding a growth engine. Thinking about this stuff early on, just like how we thought about how our own new financial tokens are integrated into a platform's ecosystem, is what turns payments from a cost center into a competitive advantage.

The Future of Global Payments Is Fast and Frictionless

Sending money across borders has always been a mess—slow, expensive, and confusing. But that’s finally changing. The old systems are giving way to new cross-border payment solutions built for the digital age: instant, transparent, and designed for people, not just banks.

If you earn, spend, or send money online, you need to understand how these moving parts work. Knowing the payment rails, the hidden costs, and the rules of the road is no longer optional. It's the key to navigating how money actually moves around the world today.

The goal is simple: make sending money as easy as sending an email. This isn't just about better tech; it's a fundamental shift that removes the old financial barriers, opening up the global economy to everyone.

A New Era for Global Earners

This shift is a game-changer for the millions of online earners, gig workers, and creators who make their living on the internet. For them, faster, cheaper payments mean getting paid what they're owed, when they need it. The days of waiting a week for a wire transfer to clear—only to have it chewed up by hidden fees—are numbered.

This isn't just a futuristic idea; it's already happening. Modern payment infrastructure is accelerating global remittances and consumer payments at a staggering pace. Systems like Europe’s TARGET Instant Payment Settlement and North America’s FedNow are already handling trillions of dollars in instant transactions. You can see the official G20 progress report to understand just how quickly global payment speeds are improving.

Klink Finance Leading the Way

This is the world Klink Finance was built for. As a global rewards platform, we empower our community to earn money by completing simple online tasks. Our whole mission—turning online time into real-world value—is only possible because we operate on these modern payment rails.

We handle all the backend complexity of global payouts so our users don't have to. By offering flexible withdrawal options and ensuring payments are fast and reliable, we connect earners to their money without the friction. It’s a perfect example of how the right cross-border payment solutions unlock real economic opportunities for people everywhere.

To see how we're positioned for what's next, read about how Klink’s infrastructure is ready for the future.

Still Have Questions? Let's Clear a Few Things Up

Diving into cross-border payment solutions can feel a bit overwhelming, whether you're building a platform or just trying to get paid on one. Here are some straightforward answers to the questions we hear most often.

What Is the Cheapest Way to Send Money Internationally?

There’s no magic bullet here—the “cheapest” way always depends on the amount, destination, and how fast you need it to get there.

Generally speaking, modern fintech platforms and e-wallets have the edge, especially for small-to-medium transfers. They're built to sidestep the old, clunky banking system, which means fewer middlemen and lower fees.

For a platform like Klink Finance, which is a global rewards app that sends out tons of small rewards, using these newer, low-cost options is non-negotiable. It’s how we make sure more of the money you earn actually ends up in your pocket, not lost to transaction costs.

Why Do International Bank Transfers Take So Long?

Ever feel like a wire transfer is moving at a snail's pace? That's because it probably is. Traditional bank wires run on an ancient system where your money has to hop between several "correspondent" banks across different countries.

Each of those handoffs is a chance for delay. Throw in different time zones, weekends, and national holidays, and the whole process can grind to a halt for days. It's exactly why newer solutions that use direct local payouts are changing the game.

At its core, the problem is that the global banking system isn't one big, connected network. It's a patchwork of individual banks, each with its own rules and hours, creating a chain of bottlenecks that every single payment has to fight its way through.

What Information Is Needed for a Cross-Border Payment?

The exact details can vary a bit, but there are a few key pieces of information you'll almost always need to provide to meet global compliance rules.

Think of it like a checklist:

Recipient’s Full Name and Address: Has to be spot-on and complete.

Bank Account Details: This is the account number (like an IBAN in Europe) and the bank's unique identifier code (like a SWIFT/BIC).

Recipient’s Bank Name and Address: The details for the bank that will receive the money.

Reason for Payment: A simple explanation like "payment for services" or "personal funds" is required by many countries.

How Do Platforms Like Klink Finance Handle Payouts to So Many Countries?

Instead of betting on a single horse, a platform like Klink Finance uses a smart mix of different cross-border payment solutions to make global payouts work smoothly. As a global rewards platform where users earn real money by playing games or completing tasks, we are connected to a whole network of payment providers, not just one.

This gives us the flexibility to pick the fastest and most cost-effective path for every single transaction. By plugging into local payment networks in different regions, we can make an international payout feel as quick and cheap as a simple domestic transfer for our users.

Ready to turn your screen time into real rewards? Klink Finance makes it simple to earn from anywhere and get paid instantly. Join our global community of earners today!

High Quality Offers,

Real Payouts

Start Earning with Klink Now!

Share Article

Related Articles

Read more, Earn more